Mathematics, 25.09.2021 01:10 yairreyes01

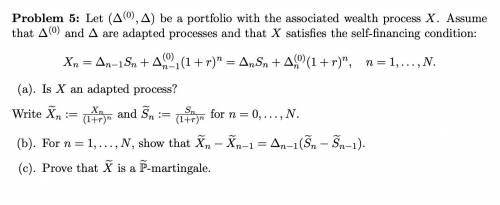

Problem 5: Let (∆(0),∆) be a portfolio with the associated wealth process X. Assume that ∆(0) and ∆ are adapted processes and that X satisfies the self-financing condition:

X =∆ S +∆(0) (1+r)n =∆ S +∆(0)(1+r)n, n=1,...,N. n n−1 n n−1 n n n

(a). Is X an adapted process?

(b). Forn=1,...,N, show thatXn−Xn−1 =∆n−1(Sn−Sn−1).

WriteXn := Xn n andSn := Sn n forn=0,...,N. (1+r) (1+r)

(c). Prove that X is a P-martingale.

(It is an intro to math finance course problem)

Answers: 1

Another question on Mathematics

Mathematics, 20.06.2019 18:04

Mrs.renoir has completed the interior portion of a quilt top measuring

Answers: 1

Mathematics, 21.06.2019 17:30

If jaime wants to find 60% of 320, which table should he use?

Answers: 1

Mathematics, 21.06.2019 21:30

(c) the diagram shows the first three shapes of a matchsticks arrangement.first shape = 3second shape = 5third shape = 7given m represents the number of matchstick used to arrange the n'th shape.(i) write a formula to represent the relation between m and n. express m as the subjectof the formula.(ii) 19 matchsticks are used to make the p'th shape. find the value of p.

Answers: 2

Mathematics, 22.06.2019 02:30

What is the output, or dependent variable of quantity? 1: x 2: f(x) 3: y

Answers: 1

You know the right answer?

Problem 5: Let (∆(0),∆) be a portfolio with the associated wealth process X. Assume that ∆(0) and ∆...

Questions

Mathematics, 20.10.2019 01:30

Mathematics, 20.10.2019 01:30

Mathematics, 20.10.2019 01:30

Mathematics, 20.10.2019 01:30

History, 20.10.2019 01:30

English, 20.10.2019 01:30

Mathematics, 20.10.2019 01:30